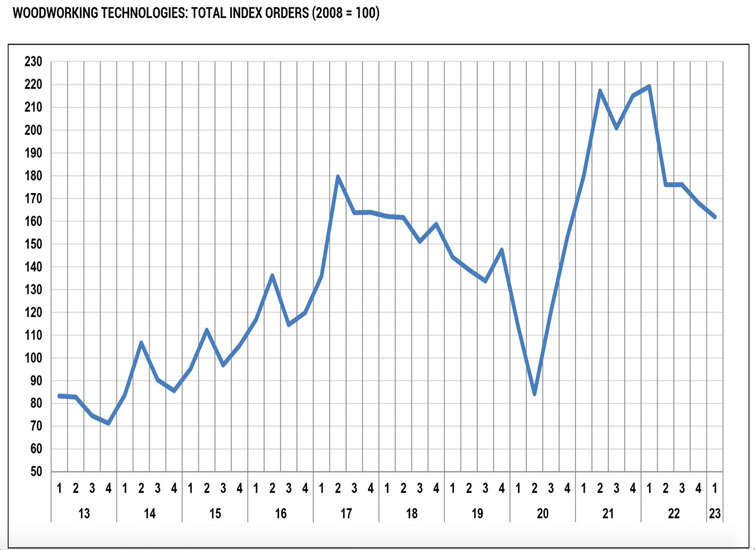

The first quarter 2023 confirmed a slowdown of orders for Italian woodworking and furniture technology. The quarterly survey by the Studies Office of Acimall (the association of Italian woodworking technology manufacturers) shows a negative trend for the fourth quarter in a row. This information must be evaluated accurately, especially considering the exceptional growth that characterized the second part of 2020 and the whole year 2021, recording a trend that has been unprecedented in the past decades. The slowdown that started in the second quarter of 2021 can be considered “physiological”, but the negative trend in the January-March 2023 period causes some worries.

In the first quarter of this year, orders recorded a 25.7 percent reduction compared to the same period of the previous year, due to decreasing demand from international markets (down by 20.6 percent) and the significant shrinkage of the domestic market (minus 38.9 percent).

It should also be noticed that the period of comparison, January-March 2022, was still an expansion phase, with significant growth rates in Italy and abroad, supported by public subsidies in many countries that, on one hand, really helped many industries overcome the consequences of the global sanitary emergency, but on the other, altered the normal evolution of the market.

The reduction of orders is reflected onto the months of ensured production, dropping from an average of 6.1 months in October-December 2022 to 5.2 months in January-March 2023.

The inflation trend – which in 2022 was in line with the economy in general – seems to be braking in the first months of 2023: the increase of sales prices for Italian wood and furniture technology was limited to 0.6 percent.

Source:ACIMALL

The opinions collected by the quality survey for the quarter under scrutiny reveal that the interviewed companies expect substantial stability of production (71 percent), while 24 percent indicates a growing trend and 5 percent a decrease. Employment is increasing according to 14 percent of the sample, stationary for 81 percent, decreasing for 5 percent. Available stocks are stable for 62 percent of the interviewees, while the remaining 38 percent is equally divided between those who indicate an increase (19 percent) and a reduction (19 percent).

The forecast survey gives an overview of the scenarios that might emerge in the short term: 38 percent of the sample expect a substantial stability of orders from the foreign markets; such orders will decrease according to 38 percent and further increase according to 24 percent. Looking at the Italian market, 57 percent of the interviewees predict substantial stability, 19 percent increasing orders and 24 percent decreasing orders.

Source:ACIMALL